Why does it take so long to sell a carbon credit?

Anyone who has worked on the sell side of the voluntary carbon market knows that selling carbon credits can feel like getting a Rube Goldberg machine to work. It’s a complex process with lots of moving parts that often takes a long time to succeed.

Earlier this year, Ecosystem Marketplace and Carbon Capital Lab launched a survey to find out what sellers are seeing in their carbon credit sales cycles. We asked 48 carbon project developers and intermediaries about how their sales conversations were progressing, when deals tend to fall apart, and why.

What we found were highly variable sales cycles, a market heavily reliant on personal relationships, and an industry in need of ongoing buyer education.

The VCM trades on relationships.

The most common sales channels are based on personal relationships – not marketplaces, formal procurement channels, or broker-facilitated deals. Instead, long-time relationships formed in prior roles are the most common way sellers meet buyers, followed closely by meeting at conferences and warm introductions from mutual acquaintances.

This heavy reliance on relationship capital for carbon credit sales could make it difficult for smaller and newer project developers to break into the market, regardless of the quality or price of their product.

Sellers are doing a lot of unpaid buyer education.

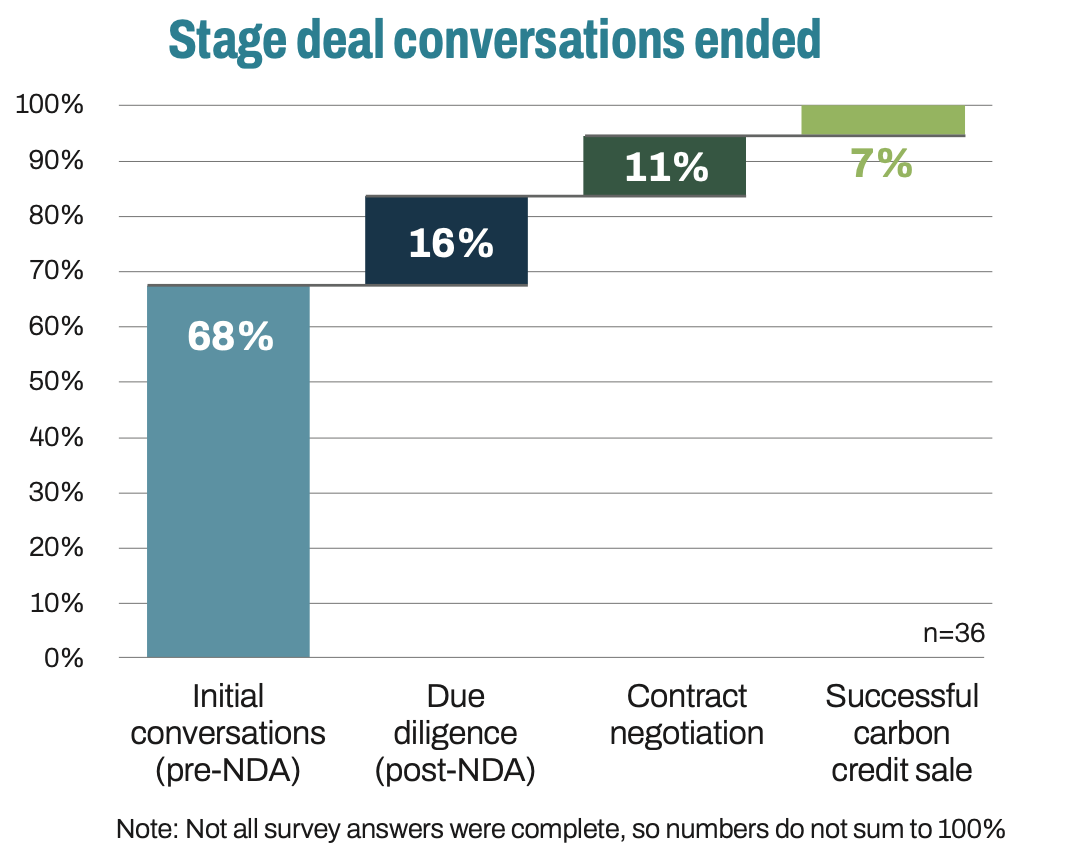

Two-thirds of sales conversations die in the very earliest stages, before formal due diligence on a carbon project even begins.

Projects told us that the most common reasons that sales conversations stall are 1) buyers’ price expectations don’t align with market realities, and 2) buyers are simply window shopping without serious intent to purchase.

Projects told us that the most common reasons that sales conversations stall are 1) buyers’ price expectations don’t align with market realities, and 2) buyers are simply window shopping without serious intent to purchase.

“Buyers are not in active procurement mode. They’re prioritizing other project types, [and] not currently thinking about carbon removals as a part of their strategy,” one survey respondent wrote.

“There was no urgency on the buyer’s end. They did not have set targets, set requirements, or set budget, and so moving the deal forward was not a priority,” wrote another respondent.

“[It’s] the wishlist versus the budget. Most of the time, buyers want mangroves at renewable pricing,” a developer told us.

Sellers are doing a lot of unpaid education in this space, using sales conversations to get potential buyers up to speed on the basics of carbon markets. That’s an expensive undertaking for project developers and retailers who may have limited runway and need to generate revenue sooner rather than later.

While multiple initiatives exist aiming to close the buyer education gap, like the Beyond Alliance, the Natural Climate Solutions Alliance, and RMI’s Carbon Markets Initiative, it seems buyers still to turn to sellers to answer their questions about the market and for price discovery.

Sales cycles are drawn out, and due diligence can become too costly to continue.

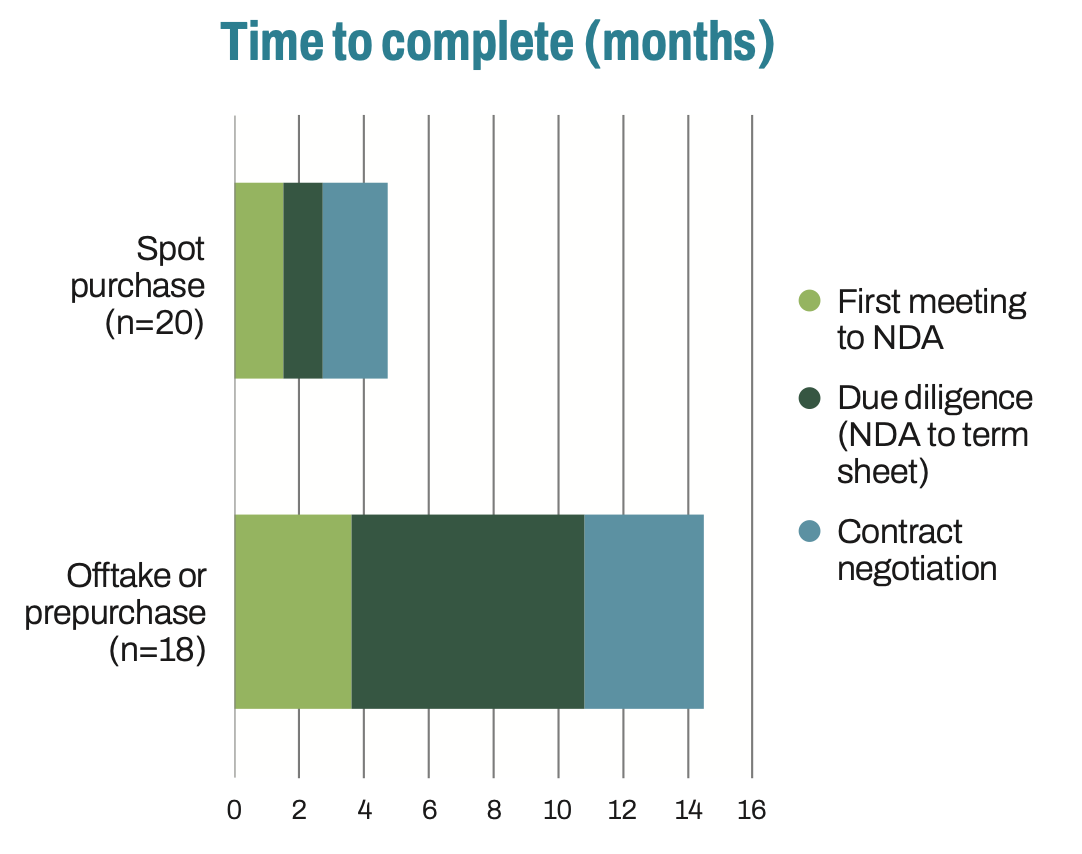

For the deals that did make it to a successful sale, spot credit sales took an average of five months to close. Offtakes took three times as long, 15 months on average, though with very wide variation between deals. The wide variance in offtake sales timelines suggests there’s still very little standardization in the due diligence process and contract structure for offtakes.

For the deals that did make it to a successful sale, spot credit sales took an average of five months to close. Offtakes took three times as long, 15 months on average, though with very wide variation between deals. The wide variance in offtake sales timelines suggests there’s still very little standardization in the due diligence process and contract structure for offtakes.

For most respondents who reported on offtake agreements, project due diligence took up the largest part of the deal cycle. Some respondents reported that buyer requests during due diligence became so costly to fulfill that they couldn’t continue with the negotiation. “Heavy negotiation without committing to the project for [the] long term. Data ask[s] become challenging to keep going back to ground and collect additional information [sic],” one developer wrote.

Other factors influencing deal timelines: Credit type, methodology, and who’s buying.

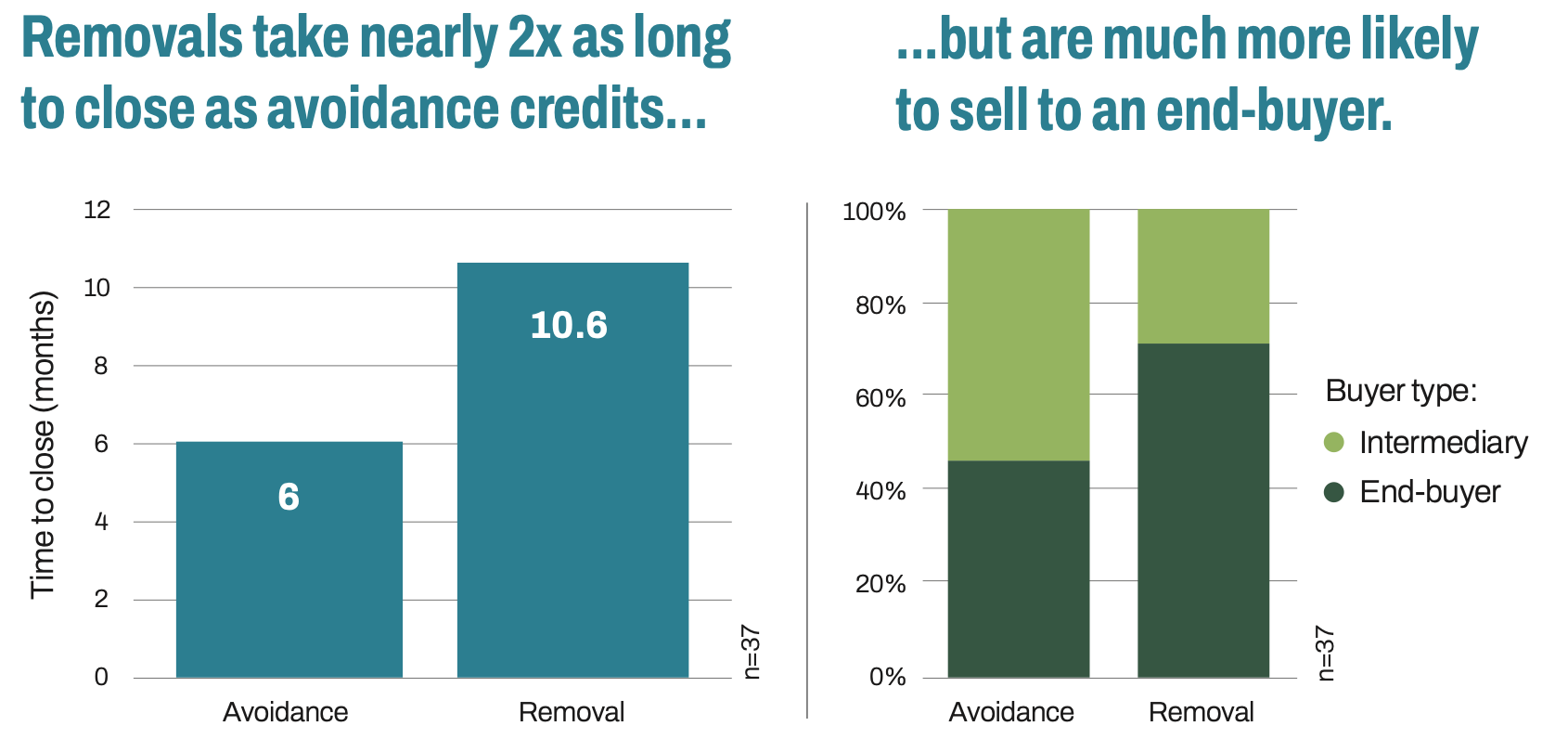

Avoidance credits close faster than removals, regardless of deal structure. For example, 80% of REDD+ sales were to intermediaries, whereas 66% of ARR sales were to end-buyers.

The prevalence of removals sales to end-buyers may be a reflection of buyer preferences. Sixty percent of removal credit sales sold via offtake rather than spot. And end-buyers are currently 2x more likely than intermediaries to sign offtake agreements, taking on the risk of longer delivery timelines but accessing larger volumes.

The prevalence of removals sales to end-buyers may be a reflection of buyer preferences. Sixty percent of removal credit sales sold via offtake rather than spot. And end-buyers are currently 2x more likely than intermediaries to sign offtake agreements, taking on the risk of longer delivery timelines but accessing larger volumes.

Standardizing due diligence processes and streamlining data collection, particularly for offtakes, could shorten deal timelines and reduce financial burden sellers experience during lengthy sales cycles.

A market where sellers spend months educating buyers, relying on old relationships, and navigating bespoke due diligence is unlikely to scale efficiently. Making transactions simpler, faster, and more predictable may be just as important to market growth as improving the credits themselves.

Please see our Reprint Guidelines for details on republishing our articles.