Opinion: ESG falling short? Low carbon funds overvalued? High integrity carbon credits offer a bridge to net zero finance

- Carbon credits can provide flexibility for more efficient and impactful use of capital where low carbon portfolios are overvalued or if ESG strategies are failing to deliver meaningful climate change mitigation.

- The financial sector’s transition to net zero should include widespread use of high integrity carbon credits (1), as a supplement to robust decarbonization targets for investment and lending.

- High integrity carbon credits provide opportunities for Financial Institutions to optimise the financial performance and environmental impact of carbon constrained portfolios and net zero strategies.

- Supporting natural climate solutions through the voluntary carbon markets enables Financial Institutions to act as a direct transmission mechanism for achieving the goals of the Paris Agreement.

Finance’s net zero conundrum

The Paris Agreement’s Article 2.1(c) describes “making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.” However, efforts by Financial Institutions (FIs) to decarbonize portfolios are hamstrung by their inability to exercise direct control over the greenhouse gas emissions of companies to which they provide finance.

FIs have some tools at hand: they can engage with companies and advocate for regulatory changes to push for progress on low carbon goals. And the Science-Based Target Initiative (SBTi) is developing standards for sectoral decarbonization, portfolio coverage and temperature ratings that will allow for evaluation of “net zero by 2050” pledges.(2)

The concept of the “value-carbon frontier”

However, the fiduciary responsibility to maximise returns means that institutional investors inevitably struggle to decarbonize investments beyond a level implied by the efforts of public policy and the real economy. As the UN Convened Net-Zero Asset Owner Alliance has stated: “To achieve net-zero investment portfolios by 2050, governments [emphasis added] must implement policies that drive the transition to a low-carbon economy.”(3)

Constructing net zero portfolios by tilting towards low-emitters and those best-in-class carbon-intensive companies transitioning to net zero has also been easier said than done. From 2016 through 2020, MSCI found that that less than a quarter of MSCI ACWI Investable Markets Index constituents decarbonized by at least 10% per year, making it virtually impossible to build broad global equity portfolios of decarbonising companies during this period, and thus raising difficult questions around accountability for achieving targets.(4)

Research from Dutch asset management firm Robeco has demonstrated empirically how attempting to increase carbon footprint reduction beyond a certain level has an adverse effect on the performance of a value investment portfolio strategy. They showed that carbon taxes up to US$100 per metric ton of CO2 equivalent, corresponding mathematically with a portfolio carbon footprint reduction of about 50%, had little effect on the characteristics and the performance of the long side of an EBITDA/EV value strategy for MSCI World stocks. However, to increase the carbon footprint reduction to 70%, the assumed carbon tax would need to rise from US$100 to an unrealistic ~US$5,000.(5)

There are, therefore, real economy constraints which result in a “value-carbon frontier” beyond which reducing the carbon footprint sacrifices financial returns in a broad-based investment portfolio.

When ESG fails to deliver and low carbon funds are over-valued

ESG funds (as opposed to low carbon funds) have faced a barrage of criticism in recent months, from the mild: that the acronym ESG jams together disparate and sometimes contradictory objectives;(6) to the damning: that the sector is rife with greenwashing and at risk of a miss-selling scandal,(7) or that funds offer little if any environmental benefit and cause actual harm by misleading investors into thinking they are addressing climate change when they are not.(8)

Genuinely low carbon strategies and investing directly in climate solutions are, of course, an effective way to reduce carbon footprints and to allocate capital to climate change mitigation. They do, however, concentrate risk in a small number of sectors, thus risking financial underperformance. Forest Trends argued in February 2021 that while continued climate policy tightening should create a positive secular trend for low carbon investments, low carbon strategies could become expensive (either because policy is insufficiently ambitious or because flow of funds into low carbon products drives valuations too high).

Since then, clean energy indexes have underperformed dramatically compared to the traditional energy sector: a 17.39% loss for the MSCI Global Alternative Energy Index in 2021 compared to an increase of 41.77% for the MSCI World Energy Index and 22.35% for the MSCI World Index.(9) JPM Asset Management’s Annual Energy Review for 2022 expected this trend to continue through 2022.(10) And in the year to 31st August 2022, the Global Alternative Energy Index was down 7.4% compared to an increase of 35.7% in the World Energy Index.

High integrity carbon credits as a bridge to net zero

Both investment managers and retail investors need the flexibility to switch out of green assets if they perceive them to be overvalued. Moreover, the sectors where emissions are hard to abate remain critical to economic growth and the transition to a carbon neutral economy. Investments in some carbon-intensive companies represent both an opportunity to finance businesses leading the way to net zero and at the same time achieve superior returns. In these scenarios investors can hold more carbon intensive portfolios and pay for credits to maintain the same carbon footprint or pay extra to achieve net zero today.(11)

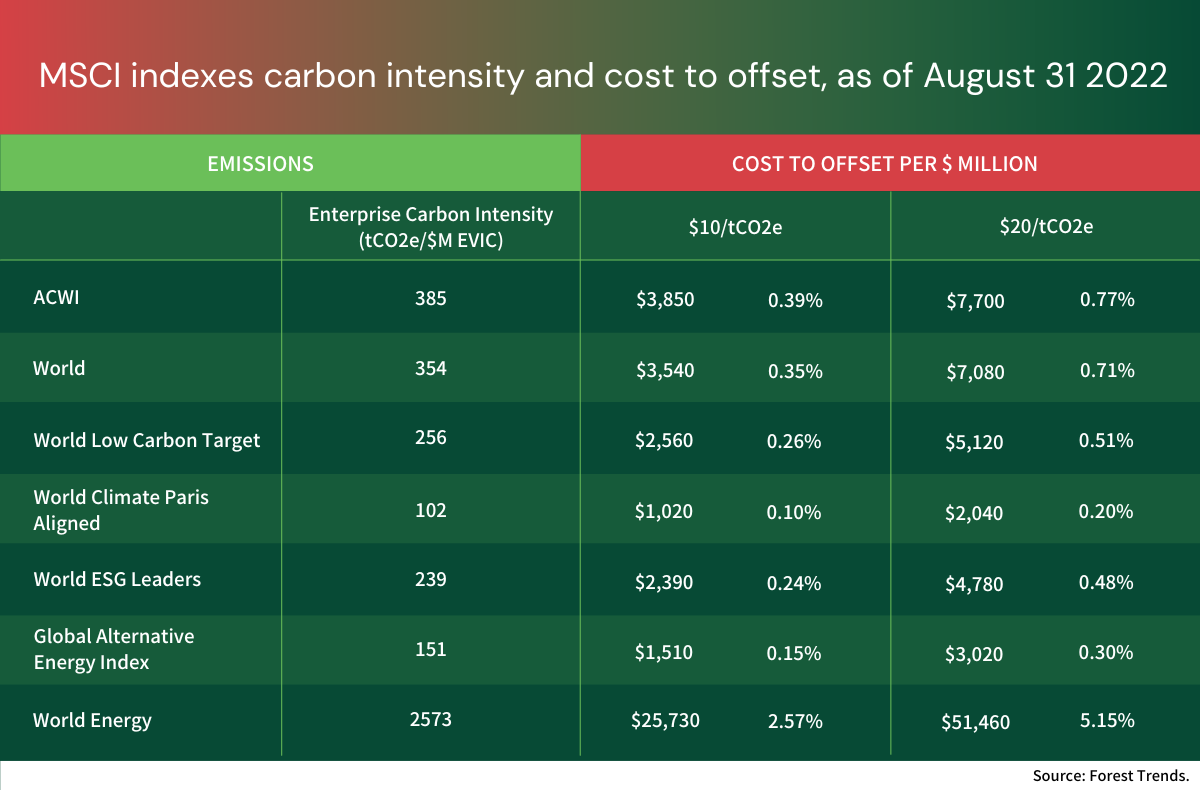

The table below shows the emissions (Scopes 1, 2 and 3) associated with a range of MSCI indexes measured as tons of CO2 equivalent per $ Million of Enterprise Value including Cash (EVIC), as at the end of August 2022. At what would currently represent a high carbon credit price of US$20, the leading MSCI ACWI index would cost 0.77% per annum to offset, the Global Alternative Energy Index 0.30% and the World Energy Index a much higher 5.15%.

However, the World Energy Index outperformed the Alternative Energy Index by 59% in 2021 and 43% in the year to 31st August 2022. Assuming a carbon credit price of $20 tCO2e, the outperformance in 2021 would have been sufficient to fully offset the difference in carbon footprint between the two indexes for fourteen years and the outperformance in the last twelve months sufficient to offset the difference for around nine years.

Carbon credits can therefore be used both to achieve net zero earlier than 2050 and to optimise the financial performance of carbon constrained investment strategies, representing a more efficient and impactful use of capital if low carbon portfolios are overvalued or if ESG strategies are failing to deliver meaningful climate change mitigation versus non-ESG benchmarks.

The potential of financial institutions as a direct transmission mechanism for Paris goals

High integrity carbon credits can allow FIs not only to follow corporate best practice but directly to support critical climate change mitigation actions.

It will be impossible to stabilize global warming below 2°C without offsets and negative emissions such as Natural Climate Solutions (which offer up to 30% of the GHG mitigation required).(12) Commitments to pay for carbon credits from FIs (as well as corporates) could enable donor governments and multilateral institutions to leverage massively more private co-funding for climate aid in developing countries and to unlock high integrity credit supply pipelines through initiatives such as the LEAF Coalition.(13)

The Natural Climate Solutions Alliance convened by the World Economic Forum and the World Business Council for Sustainable Development has developed an NCS Investment Accelerator, supported by several corporates, which aims to go beyond internal decarbonization trajectories by investing in high integrity credits to offset residual emissions on an annual basis.(14) FIs and their ethically oriented clients can do the same. Indeed, use of carbon credits by FIs would reinforce competitive pressure for corporate action, not least because FIs would have no need to offset the carbon footprint of investee companies which have already offset emissions beyond their value chain.

Supporting the development of a liquid market in high integrity carbon credits could allow FIs to go beyond the “value-carbon frontier” in global financial markets implied by policy signals in the real economy, and to act as a direct transmission mechanism for achieving the goals of the Paris Agreement.

(1) For detail on what constitutes “high integrity” see:

The Tropical Forest Integrity Guide https://tfciguide.org/wp-content/uploads/2022/07/TFCI-Guide-English.pdf

The Integrity Council for the Voluntary Carbon Market https://icvcm.org/

(2) Financial Sector Science-Based Targets Guidance Version 1.0 February 2022. https://sciencebasedtargets.org/resources/files/Financial-Sector-Science-Based-Targets-Guidance.pdf

(3) UN Convened Net- Zero Asset Owner Alliance. Position Paper on Governmental Carbon Pricing. June 22

https://www.unepfi.org/wordpress/wp-content/uploads/2022/06/NZAOA_Governmental-Carbon-Pricing.pdf

(4) MSCI. Constructing Net-Zero Portfolios: Three Approaches. September 2021. https://www.msci.com/www/blog-posts/constructing-net-zero/02768215423

(5) Robeco. December 2021. Factoring carbon taxes into a Value strategy

https://www.robeco.com/uk/insights/2021/12/factoring-carbon-taxes-into-a-value-strategy.html

And see: Blitz, D., and Hoogteijling, T., November 2021, “Carbon-tax-adjusted value”, working paper.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3974773

(6) Financial Times. Jonathan Guthrie. April 2022. ESG is a category error that needs unbundling

https://www.ft.com/content/c8b11672-4847-44ae-b132-788cb2383a2c?shareType=nongift

(7) Financial Times. Laurence Fletcher and Joshua Oliver. February 2022. Green investing: the risk of a new mis-selling scandal

https://on.ft.com/3s3UHUu ; https://on.ft.com/3Nu8r3m

(8) Tariq Fancy. The Secret Diary of a Sustainable Investor.

https://www.dropbox.com/s/bvskswxwkro41rh/The%20Secret%20Diary%20of%20a%20Sustainable%20Investor%20-%20Tariq%20Fancy.pdf?dl=0

(9) https://www.msci.com/documents/10199/de6dfd90-3fcd-42f0-aaf9-4b3565462b5a; https://www.msci.com/documents/10199/40bd4fec-eaf0-4a1b-bfc3-8ed5c154fe3c

(10) JPMorgan Asset Management Annual Energy Review 2022

https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/2022-energy-paper/executive-summary-amv.pdf

See also

It’s Not Easy Being Green: Why Is ESG Underperforming In 2022? Taylor Tepper. Forbes Advisor.

https://www.forbes.com/advisor/investing/why-is-esg-underperforming/

Divesting fossil fuel stocks? That’s so last year. Merryn Somerset Webb. Financial Times. February 2022

https://on.ft.com/350obcR

(11) The Net Zero Transition and Offsetting of Carbon Intensity in Retail Investment Portfolios. Rupert Edwards. Forest Trends

(12) Griscom et al. 7 January 2020. National mitigation potential from natural climate solutions in the tropics

https://royalsocietypublishing.org/doi/10.1098/rstb.2019.0126

(13) https://leafcoalition.org/

(14) NCS Alliance Investment Accelerator

https://www.wbcsd.org/Programs/Climate-and-Energy/Climate/Natural-Climate-Solutions/The-NCS-Investment-Accelerator

https://www.weforum.org/natural-climate-solutions-alliance/ncs-investment-accelerator

Please see our Reprint Guidelines for details on republishing our articles.