Opinion Nine Steps Towards Doubling The Value Of US Mitigation Markets

There is significant movement in the ecosystem market space as a new presidential memorandum seeks to ramp up private investment in conservation and a recent analysis values the marketplace at $100 billion. To help capitalize on this movement a market analyst offers a brief list of recommendations for the rule makers – by William Coleman

21 December 2015 | Recent research shows rapid growth for the U.S. compensatory mitigation credit (CMC) marketplace, placing its value at $100 billion. And researchers determined this figure before the administration of President Barack Obama released a presidential memorandum, which intends to aggressively expand these markets by encouraging new levels of private investment in compensatory mitigation projects.

With both of these developments in mind, there are a series of deliberate steps regulating agencies can take to grow the markets while at the same time rebuilding important ecosystem services nationwide.

$100 Billion and Growing

Two recent findings identified the billion dollar value of mitigation credits. First, Eco-Asset Solutions & Innovations, a California-based firm focused on mitigation credit development and valuation, undertook a detailed effort in 2014 to collect mitigation credit price information. This highlighted real price trends for wetlands, conservation and water quality credits drawn from bid results, contracts, news stories and other archived references to real-world mitigation credit pricing.

This dataset has helped overcome the lack of transparency that has plagued the CMC marketplace from the beginning – more than 30 years ago, when the market was solely comprised of wetland credits. The data sheds light on historic CMC price trends and regional price variations. This allows developers to know what to expect in terms of return on investment, and buyers to know what to expect in terms of overall project environmental costs.

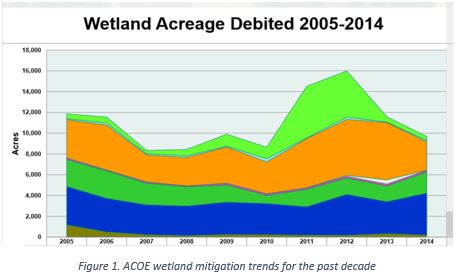

Second, the U.S. Army Corps of Engineers (ACOE), which oversees U.S. wetlands mitigation banking activity, presented information about the volume of wetland and stream mitigation credit activity from 2005 through 2014 at this year’s National Mitigation Banking Association annual meeting in Orlando. The Corps showed (Fig. 1) that an average of about 11,000 credits per year have been debited from approved mitigation bank totals over the past decade. This information allows us to see, for the first time, the average annual demand for wetland mitigation credits based on the prior ten-year period.

With these two datasets in hand, it became possible to estimate the annual transaction value for wetland credits in the U.S. The mitigation credit price data gives us an average wetland credit value of $95,000 for the prior ten year period. The average credit value is dependent on the number of price points in the dataset, as well as the recorded value for each mitigation credit trading hands. The $95,000 figure is derived from over 130 price points representing transactions from 2005-2014. If 11,000 credits trade hands each year, at an average value of $95,000 each, the annual transaction value for wetland mitigation credits is over $1 billion in the current timeframe.

Taking the next step, we can estimate the size of the entire wetland mitigation credit market based on the number of approved mitigation credits held by U.S. landowners. That number, which is 775,000, comes from the ACOE RIBITS website. Multiplying the number of approved credits reported in RIBITS by the 10-year average wetland credit value, we see that the wetland mitigation credit market is about $74 billion in size. If we use a more current, 3-year average price for wetland credits – $144,000 – the market can be valued at $112 billion. This reflects the increasing significance of wetland mitigation activity in recent years.

The midpoint between these two market value estimates – the 10-year average vs. the 3-year average – is $93 billion. If we add in the value of the U.S. conservation credit market, species and habitat credits, using the same approach described above, another $6 billion in credit value comes into view. This brings CMC market value to $99 billion. Water quality credits – another form of compensatory mitigation – have been rapidly proliferating across the country, in such places as the Ohio River Basin and the Chesapeake Bay. Even though their value isn’t calculated at present there is little doubt that total compensatory mitigation credit marketplace is at least $100 billion strong.

Preparing for the Next $100 Billion

The Obama administration’s memorandum directs all U.S. natural resource agencies to foster opportunities for businesses to achieve restoration and conservation objectives. The list of agencies addressed in the Memorandum includes the Environmental Protection Agency (EPA), Departments of Agriculture (USDA) (Forest Service, Natural Resource Conservation Service), Interior (DOI) (Fish & Wildlife Service, Bureau of Land Management, Office of Surface Mines) and Defense (Army Corps of Engineers), as well as the National Oceanic & Atmospheric Administration (National Marine Fisheries Service).

Agencies are instructed to encourage advance compensation, including mitigation bank-based approaches. They are encouraged to collaborate so that integrated policies and guidelines will incentivize private investments needed to produce successful advance mitigation compensation for future development impacts.

The agencies have been gradually moving in this direction anyway. The USDA Office of the Chief Economist established an Office of Environmental Markets as directed by the 2008 Farm Bill. In 2014, the DOI’s Energy and Climate Task Force presented Interior Secretary Sally Jewell with a report summarizing strategies for improving the mitigation policies and practices of Interior Department. And this year the EPA has been making efforts to expand water quality markets and trading in concert with the USDA. The EPA also committed to develop an environmental markets data layer for EnviroAtlas, the agency’s ecosystem services management tool.

Progressive as these steps have been over the past few years, the memorandum now directs agencies to create a new set of common strategies and tools facilitating private sector investment in mitigation banking. Landowners – farmers and ranchers as well as business and industry – will take notice. The net effect will likely be to quickly accelerate the development of compensatory mitigation projects. This will lead to an unexpectedly large number of new mitigation credits coming to market in a few years’ time.

These developments will also result in a dramatic increase in protection, enhancement, restoration and creation (PERC) of badly needed, sustainable ecosystem services. These developments will also affect our understanding of ecosystem service values. Nothing sheds light on value more quickly than direct market price signals.

With the above in mind, in order to see results as soon as possible, agencies may want to consider the following steps towards achieving the goals of the president’s memo. If the goals can be met, the next $100 billion in value for the U.S. mitigation credit marketplace will quickly be realized.

- Update RIBITS so mitigation credit data is current, complete and comprehensive. Rumors abound that current RIBITS data is out of date; some regional offices of the Corps are believed to be slow to report results of mitigation credit project development or completion. Other rumors suggest that RIBITS will soon incorporate water quality credits. If so, this is excellent news. RIBITS should be the centralized national dataset accommodating all compensatory mitigation credit activity (including future soil and biomass carbon sequestration credits, especially if these are ‘stacked’ with more traditional mitigation credit types).

- Expand and systematize wetland, conservation and water quality mitigation programs so they are uniform from state to state. Several states still do not have even basic wetland mitigation strategies in place. Other states prefer In Lieu Fee programs to market-based programs. Still other states blend in lieu fee and market programs so it becomes difficult to understand how private sector incentives can really work. Finally, water quality mitigation programs deserve to be consistently applied so there is a national market for credits similar to wetlands and conservation credits.

- Expand conservation credit markets to include candidate species under the Endangered Species Act. Current species mitigation programs focus on threatened or endangered species listed under the federal Endangered Species Act or state equivalents. Making candidate species available for mitigation accomplishes several things. This would:

- Diminish the chance of a candidate species needing to be listed as threatened or endangered in the future

- Encourage PERC for candidate species habitats, building back ecosystem richness and related ecosystem services

- Recruit more states to participate in conservation banking projects

- Build additional robustness into the conservation credits market segment

- Make the effort to capture and represent all CMC asking prices. The CMC marketplace has been a seller’s market from the beginning. Sellers have protected the prices of their credit offerings to prevent being undersold. The result has been high price volatility. In addition, sellers have been relatively few and the availability of credits has not always been widely known. Poor market transparency has meant that buyers could not always find what they needed to comply with permit obligations. Nor could buyers predict a reasonable price for the credits they were required to purchase. These problems disappear as soon as mitigation credit prices, and credit availability, is widely known.

- Make public the results of all government agency CMC bid requests. Buyers, especially government entities such as transportation departments, often announce Requests for Bids in advance of projects that are likely to have unavoidable environmental impacts. These bid requests are part of the public record. But the results of the bidding process are not made public, probably at the request of sellers who want to protect their pricing strategies from nearby competition. S. Department of Transportation, for example, will not release bid results without a Freedom of Information request. Such extra steps discourage improved market transparency and extend the plight of disadvantaged CMC buyers.

- Provide for public-private CMC partnerships within or adjacent to National Forests. Rehabilitation of forested landscapes is an increasingly critical component of natural resource / regional ecosystem services management. Catastrophic fires have seriously compromised ecological productivity in large portions of the U.S., possibly for centuries in areas where soil, water and biodiversity resources have been seriously debilitated. Public-private partnerships can minimize the recovery time from burn zone areas. However, current incentive-based recovery of burn zones is complicated by the boundaries delineating public vs. private forested lands. This boundary is usually artificial where ecosystems are concerned. Watersheds, for example, often include both public and private properties. Species may range freely across such boundaries. S. Forest Service should study incentive-based rehabilitation mechanisms that simultaneously benefit both public and private lands in burn zones at risk for rapid depletion of ecosystem services.

- Standardize CMC accounting and auditing processes. Landowners can earn CMCs without having to formally declare a mitigation banking project. All CMCs require conservation easements (and attendant endowment funds) to ensure long term management in the public interest. Conservation easements serve as the basis for awarding CMCs. Once signed, easements are typically registered in the County Surveyors office. But that may be all that’s required of a landowner in the case of an informal, non-bank CMC project. Agencies have a good record reviewing formal mitigation bank conservation easements and CMC disbursements to make sure authorized mitigation credits are tracked. But non-bank conservation easements and credit disbursements can go unattended. Over time this inattention can lead to accounting problems as landowners gradually sell informal, non-bank mitigation credits. How many credits have been sold? Have any credits been resold; if so, to whom? Could credits have been sold twice for the same purpose? Uniform accounting and audit processes are called for to ensure informal, non-bank CMCs are treated the same as formal bank CMCs.

- Provide for investment and/or resale of unused CMCs. Agencies seeking to minimize mitigation credit tracking and accounting burdens have discouraged the resale of these credits. In some cases this leads to higher costs for credit buyers. For example, a buyer can purchase a number of credits to offset unavoidable project impacts, only to learn later on that fewer credits than expected were needed to satisfy compliance obligations. This leaves the buyer with leftover credits. If unused credits cannot be resold the buyer is left with a stranded investment. Further, investors should be able to buy and bank credits for later sale the same way NGOs buy and retire mitigation credits. Mitigation credits are ecological assets, commodities similar to other forms of commercial paper. Market privileges available to other paper commodities should also be available to CMCs.

- Widely educate potential market participants, especially landowners, about the rationale, mechanics and prospective value of CMC projects. Farmers & ranchers, business & industry are still largely unaware of incentive-based CMC programs. Ranchers, for example, are often suspicious of conservation easements. They often do not understand that property ownership doesn’t change with a conservation easement, and that current, compatible uses can be accommodated alongside dedication of acres to long term ecological outcomes. Industry is largely unaware of the economics of developing CMCs on underutilized properties. Investors are actively discouraged from participating in CMC markets. The net effect has been to constrict growth of the CMC marketplace-despite its having achieved the $100 billion milestone.

By implementing the above steps agencies will commit to a persistent, widespread effort to recruit new market participants, helping achieve the next $100 billion in CMC value. Not only will this underscore the relevance and value of the environmental marketplace but it will facilitate quality-of-life outcomes related to preservation, enhancement, restoration and creation of ecosystem services on private lands.

Please see our Reprint Guidelines for details on republishing our articles.